OpenAI's health chief says bet on the models 🎲, CMS moves to ban RPM vendors 🚫, 340B quietly hits $100B 💊

⚡ Around the Wards

OpenAI’s health-AI chief says “bet on the models getting better” — the strategy is architect for the model you’ll have in 12 months, not the one you have today. The uncomfortable corollary for point-solution builders is below.

🔮 within a year, “we fine-tuned a model” stops being a pitch and starts being a liability.

CMS proposes banning third-party vendors from delivering Medicare RPM — the codes survive; the RPM-as-a-service business model doesn’t. Comments due mid-September, effective Jan 1, 2027.

HCA warns treating the newly uninsured will trim up to $1.2B in 2026 profit — HCA raised its expected hit to $1–1.2B (from $600–900M), the first hard number on ACA-subsidy fallout, and it’s the budget every health-system tech deal now has to survive.

Pathology is the specialty clinical AI forgot — a new July 15 NEJM AI Perspective (F.-Y. Su et al.) argues the blocker isn’t model quality, it’s deployment, regulation, and infrastructure. That’s a builder problem, not a research one.

🎧 Podcast: Relentless Health Value, Ep. 520 — an Annals study found 43% of the top-20 generics cost more out-of-pocket through insurance than the GoodRx cash price (≈79% while you’re in the deductible). Sometimes the plumbing you’re building around is the problem.

🧭 The Curbside

“Can a primary-care doc now rule out Alzheimer’s as well as a specialist?”

Short answer: For ruling it out, increasingly yes — with a blood test, not a scan.

What changed / Evidence: Data presented at AAIC shows a p-tau217 blood test (PrecivityAD2) let PCPs match specialists at ruling out amyloid pathology — PCP diagnostic accuracy jumped from ~62% to ~88% with the test, and clinicians altered their diagnosis in about 30% of patients (most often to rule Alzheimer’s out).

Builder read / Watchout: The diagnostic frontier is moving into primary care, where the interpretation layer is thinnest. The wedge isn’t the assay — it’s the triage logic that tells a PCP what to do with a positive. Don’t overclaim: this is rule-out and risk-stratification, not a diagnosis on its own.

“Is my patient-facing web app a wiretapping lawsuit waiting to happen?”

Short answer: If it loads third-party trackers on any page that touches health info, it’s exposed.

What changed / Evidence: A wave of CIPA (California wiretapping law) claims is now extracting settlements from digital-health companies over web-tracking pixels — several are quietly paying.

Builder read / Watchout: This is a plaintiff-lawyer business model, not a one-off. Audit every marketing pixel, session-replay script, and analytics tag on any surface that mentions a condition before you ship consumer health web apps.

😤 “That’s a lawyer problem, not a builder problem.” It stops being a lawyer problem the first time a demand letter names your

<head>tag.

🔬 The Big Thing

Bet on the models getting better — and lose the bet you didn’t know you were making.

Karan Singhal, who leads health AI at OpenAI, laid out the whole strategy in one line: bet on the models getting better.

His point is that health systems keep architecting around today’s model — its context window, its failure modes, its price. Design for the model you’ll have in a year instead.

He’s not wrong about the trajectory. This week’s generation runs roughly 25x cheaper than the last one at comparable quality, and the curve isn’t flattening.

Here’s the bet a builder makes without noticing: every line of code you write to compensate for a current model limitation is a depreciating asset. The model improves, and your clever workaround becomes dead weight.

The sharpest framing I heard all week came from a founder automating FDA submissions: “We think about the models as an engine. We’re building the car.” Stop tuning the engine you rent. Build the thing around it that stays valuable as the engine improves — the workflow, the trust, the domain judgment.

But there’s a second bet hiding underneath, and it cuts the other way. If capability alone decided outcomes, spending would already be falling. It isn’t.

A new NEJM AI piece from David Blumenthal and Meredith Rosenthal argues the near-term effect of AI on national health spending is set by payment policy, not model quality. Prospective budgets and value-based contracts decide whether a smarter model saves money or just does more billable things faster.

So the real builder question isn’t “will the model get better?” It obviously will. It’s “when the engine everyone rents is this good, what do I own that they don’t?” The answer is the same thesis this newsletter keeps landing on: the workflow no one else understands, and the judgment of someone who’s actually held the pen.

😤 “This is just OpenAI telling me to buy OpenAI.” Fair — the health chief of a foundation-model company saying “bet on foundation models” is not a neutral referee, and he never flags the conflict. But the depreciation math is true no matter whose model you rent. Discount the salesman; keep the arithmetic.

😤 “So domain experts just get replaced faster.” Backwards. The cheaper the engine, the more the scarce input is the person who knows which car to build. You don’t compete with the model. You aim it.

😤 “’Build the car, not the engine’ is a nice metaphor that pays no bills.” You should try it, then. Ship one workflow that stays useful after the next model drop and you’ll feel the difference between renting capability and owning a process.

❓ If the model is a commodity and the moat is trust plus workflow, what’s the smallest durable thing a solo clinician-builder can own that a foundation-model lab can’t casually eat next quarter? I keep circling the answer and can’t quite name it.

🧪 Try the interactive — two takes on today’s RPM-vendor-ban story, both built with real CMS Medicare Part B data:

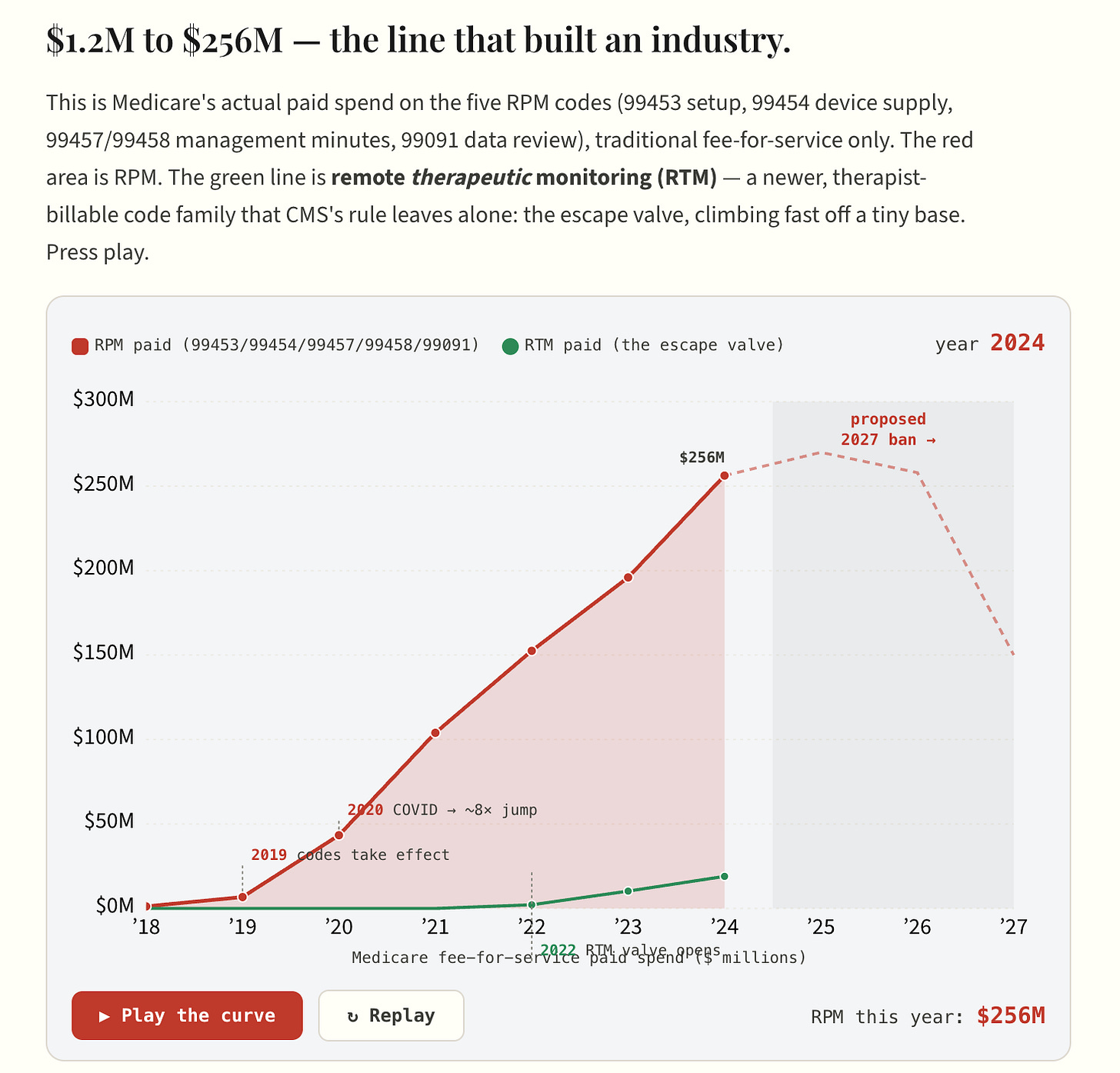

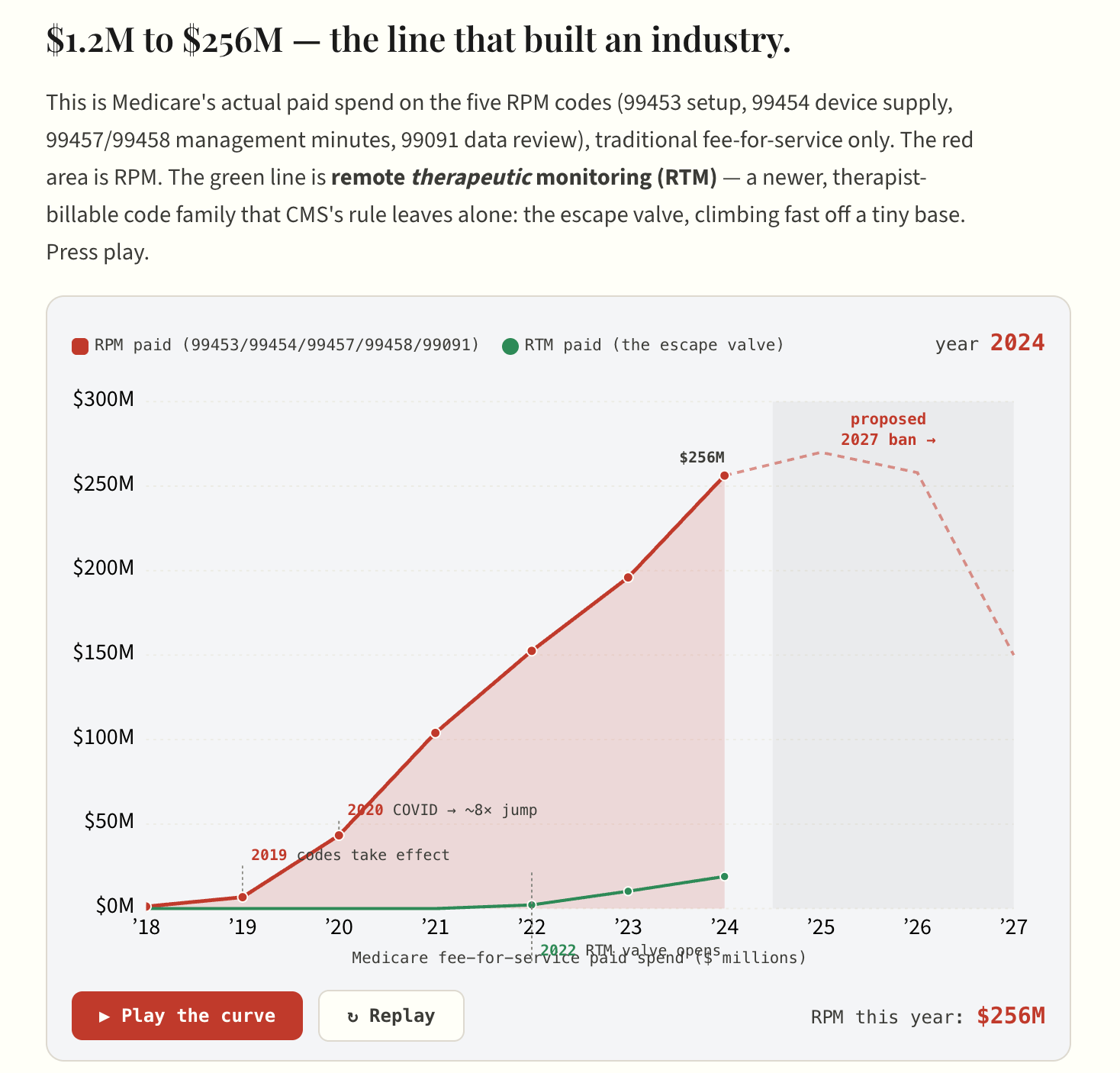

The Code That Outgrew Its Model — Medicare’s RPM billing went from $1.2M in 2018 to $256M in 2024, a 210× run; watch the hockey stick draw itself, then see where the 2027 vendor ban lands.

The Vendor Fingerprint — every state plotted by the two fingerprints of the vendor model: how concentrated the billing is (patients per provider) and how intensely each patient is billed (device-months per patient).

📡 Builder’s Radar

CMS wants to ban the RPM business model — not the RPM codes.

CMS’s CY2027 proposed rule would stop paying when a third-party vendor delivers remote patient monitoring — the codes (99453/99454/99457) stay, but the pay-per-patient vendor model that built the category becomes non-compliant.

RPM payments topped $500M in 2024, almost all of it flowing through exactly the arrangement CMS is targeting.

The signal underneath: CMS wants to pay for digital health as a clinical service a provider delivers, not a product a vendor rents to a practice. Remote therapeutic monitoring (RTM, codes 98975–98981, therapist-billable) is the escape valve — for now.

😤 “They’ll never finalize it.” Maybe. But the comment window closes in September and the direction is unambiguous. Read the rule before you raise your next round on RPM MRR.

🔮 My bet: by the time this finalizes, at least two of the big RPM-as-a-service companies will have rebranded as RTM or pivoted to a per-provider SaaS license. The regulatory path is the product strategy now.

R1 says the revenue cycle needs an operating system — and built one.

R1 is scaling “Phare,” pitched as the first revenue-cycle operating system (launched late 2025, profiled by Hospitalogy this week as it adds new capabilities): one platform across 1,500+ payers, claiming 97% autonomous coding. Hospitals lost roughly $48B to denials in 2025, so the pain is real.

“Epic for the revenue cycle” is the play — and if it lands, every point-solution RCM startup just became a feature. The infrastructure layer keeps eating the tools built on top of it.

😤 “97% autonomous coding is a marketing number.” Almost certainly. The 3% is where the audit risk, the DRG downgrades, and the compliance exposure all live — and that 3% is the whole job.

Pathology: the specialty AI forgot.

A new NEJM AI Perspective argues pathology lags other specialties in clinical-AI adoption (F.-Y. Su et al., July 15) not because the models are worse, but because deployment, regulation, and lab infrastructure are the bottleneck.

The recurring pattern of 2026: the hard part stopped being the model and became everything around it. That’s not a reason to wait — it’s the map of where the buildable problems actually are.

💡 80/20: If you want an underbuilt corner of clinical AI, look where the science is ready and the plumbing isn’t. Pathology’s whole-slide pipeline is a plumbing problem wearing a research disguise.

HCA puts a number on the coverage cliff: $1.2B.

HCA told investors that treating more uninsured patients will cut 2026 profit by $1–1.2B — up from an earlier $600–900M estimate — as enhanced ACA subsidies expire.

Why a builder should care: this is the number that governs every “nice to have” tech deal for the next 18 months. When margin compresses, tools that demonstrably reduce cost survive procurement and tools that “improve experience” die in committee.

🔮 My bet: the 2027 budget cycle kills more clinical-AI pilots than any accuracy failure does. “What number does this move” stops being a good question and becomes the only question.

Ultra-shorts

Another senior Epic AI departure — the second in a month, a 20-year veteran on the AI side. One exit is noise; two in four weeks around a leadership transition is a pattern worth watching if you build on the Epic ecosystem.

Kaiser nurses protested the company’s AI strategy outside the AHA Leadership Summit — the union fight over workflow AI has moved from the bargaining table to the CEO’s conference stage. Deployment consent is now a labor issue, not just a governance one.

Neko Health raised $700M to enter the US — the largest round yet in cash-pay whole-body scanning, opening in New York. The category’s moat is no longer the scanner; it’s what you do with a healthy person’s incidental findings.

The bipartisan “Patients First Act” would tie Medicare physician pay to inflation (MEI) — introduced within a day of the CY2027 fee-schedule draft. If indexing ever passes, it reshapes the payment vehicle every telehealth and RPM rate rides on.

Niels Rogge (ML Engineer, Hugging Face) flagged Bonsai 27B — reportedly the first 27B-class model to run on a phone at ~3.9GB with most of its intelligence intact. The clinical read: on-device inference for PHI without a cloud round-trip keeps getting more real, which is the whole ballgame for building on patient data you can’t send anywhere.

Abigail Watson (interoperability engineer) shared a first draft of a Care Commons EHR software manual + certification attestation — generated in CI and meant to be read by LLMs — for the 2026 CMS Connectathon. Machine-authored conformance docs for machine consumers is a small, concrete glimpse of where interop tooling is heading.

🎙️ From the Pods

🎙️ NEJM AI Grand Rounds — “Weave’s Brandon Rice on Rebuilding Drug Regulation with AI”

The durable moat for a clinical-AI startup isn’t a fine-tuned model — it’s trust plus a platform built “with headroom” that assumes the base models keep improving. An IND package costs ~$500K and months of pure information-transformation work, which is near-ideal LLM territory.

💡 Builder take: Stop shipping code that compensates for today’s model limits; build the workflow layer that gets more valuable as the engine improves.

🔇 Speaker Blindspot: Streetlight effect — he anchors the value on the visible, measurable paperwork cost (the $500K IND) while conceding the real rate-limiter, establishing causality in trials, is uncompressible. And “multiple customers got FDA approvals” is a win with no denominator — survivorship bias — especially since INDs already clear >90% of the time.

🎙️ Relentless Health Value — Ep. 520, “Cash-Pay Generic Drugs Are a Functioning Market”

Multi-source generics are one of the few genuinely competitive markets in US healthcare — and routing them through insurance often makes them more expensive. PBMs reportedly extract ~$41 of every $100 spent on generics that cost cents to make.

💡 Builder take: Before you build affordability tooling, ask whether a functioning market already exists. For generics, the win is a cash rail that bypasses adjudication, not another benefit that pools risk onto a $3 drug.

🔇 Speaker Blindspot: Composition fallacy — the host carefully carves out multi-source generics as the one segment that works, then lets “the invisible hand works” energy generalize toward the rest of the drug channel, where single-source and specialty economics behave nothing like this.

🎙️ The Gist Healthcare Podcast — Wednesday, July 15, 2026

New CMS data shows ACO REACH saved Medicare roughly $1B net in PY2024, with 96 of 115 ACOs earning savings — and the model sunsets Dec 31, replaced by the LEAD model on Jan 1.

💡 Builder take: The value-based scaffolding just changed shape again. If your tool’s ROI story depends on a specific shared-savings model, tie it to the mechanism (attribution, risk, quality capture), not the program name that keeps getting rebranded.

🔇 Speaker Blindspot: Survivorship framing — a “$1B saved” headline counts the ACOs that stayed in and earned savings, not the ones that dropped out along the way, which is exactly the denominator that tells you whether the model actually works.

💰 Money Plumbing

340B just crossed $100B — and almost no clinician-builder knows it exists.

340B-covered entities purchased $100B in drugs in CY2025, up 22.8% year over year, per HRSA’s own figures. Against a list value near $179.5B, that’s roughly an $80B discount spread — a program now larger than the entire Medicaid drug benefit.

Here’s the mechanism in dollars: a safety-net hospital buys Keytruda near $7,000/vial under 340B, bills Medicare at ASP+6% (~$10,600), and keeps ~$3,600 per vial. Five hundred vials of one drug is $1.8M in spread. For many DSH hospitals, that spread is the margin line.

The program is simultaneously under attack from three directions — CMS proposing to cut 340B reimbursement to ASP−33.4% in the hospital outpatient setting, drugmakers restricting contract-pharmacy access, and Congress circling. That collision of a $100B flow and a shifting rulebook is a software problem hiding in plain sight.

💡 Builder move: The buildable surfaces are 340B compliance/audit tooling, contract-pharmacy network management as manufacturers tighten access, and site-of-care optimization that models the HOPD-vs-office spread before CMS’s cut lands. Start on public HRSA data — no PHI required to prototype the economics.

💡 BTW: Karan Singhal, the OpenAI health lead telling systems to bet on the models, is the researcher who built Med-PaLM at Google — the first model to hit expert-level on US medical-licensing questions — then left to build health AI at OpenAI, where he also runs the “AGI Benefits” team. The person urging everyone to bet on the models getting better has spent his entire career being the reason they do. (He was named to the 2026 Time100 Health list for it.)

Keep building out there - Kevin & AI